.png?width=844&height=471&name=Blog%20-%20Prequal%20vs%20Pre-Approval%20vs%20Fully%20Underwritten%20(1).png)

Watch the YouTube video if you're a visual learner

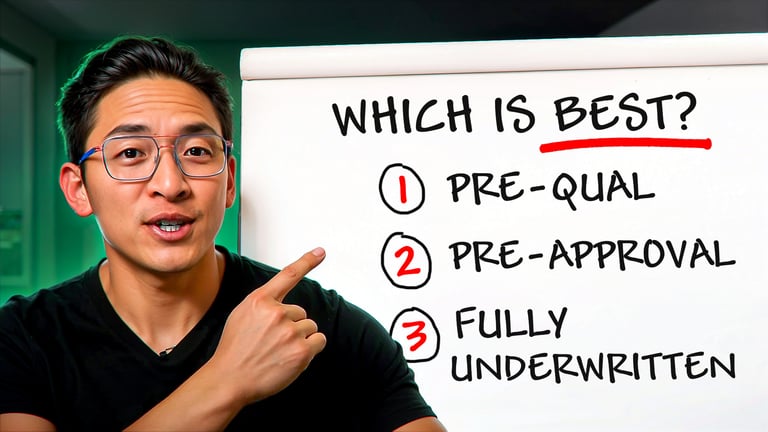

What are these fancy words?

When you're diving into the homebuying process, you'll hear terms like pre-qualification, pre-approval, and fully underwritten pre-approval tossed around a lot. But what do they actually mean, and more importantly, which one do YOU need?

Level 1: Pre-Qualification (The Casual Starting Line)

Think of pre-qualification like dipping your toe into the water. It’s a quick estimate of what you might be able to afford based on self-reported information.

✅ Pros:

-

Fast and easy (usually within minutes)

-

Good for early exploration

-

No need to upload documents

❌ Cons:

-

Based on unverified info (self-reported)

-

Not taken seriously by most real estate agents or sellers

Best for: Buyers who are just getting started and are 1–2+ years away from seriously house hunting.

Pro Tip: If you’re at this stage, check out my Home Affordability Calculator I created. It’s more useful than most generic tools out there and helps you understand how different variables impact what you can afford.

Level 2: Pre-Approval (The Smart Next Step)

A pre-approval is the next level up. Now your lender actually verifies your income, credit, and assets. It’s more work upfront but opens a lot more doors.

✅ Pros:

-

Stronger than a pre-qualification

-

Makes real estate agents take you seriously

-

Many lenders offer a soft credit pull (no score impact!)

❌ Cons:

-

Requires uploading financial documents

-

Takes more upfront time and effort

Best for: Anyone planning to buy within the next 6 months.

My Takeaway: If your lease ends in a few months or you’ve already been researching homes seriously, skip the pre-qual and go straight for the pre-approval with a soft credit check. It’s like doing your homework before the test.

Level 3: Fully Underwritten Pre-Approval (The Gold Standard)

This is the most powerful mortgage approval you can get. Your file is reviewed not just by your loan officer, but also by an underwriter, who’s the real decision-maker when it comes to approving loans.

✅ Pros:

-

Treated almost like a cash offer in competitive markets

-

Builds seller confidence

-

Reduces surprises and delays later in the process

❌ Cons:

-

Takes the most time upfront

-

You’ll need to provide complete documentation early on

Best for:

-

Buyers in competitive markets (like Southern California)

-

Self-employed individuals

-

Buyers with complex finances (multiple jobs, rental income, etc.)

Pro Tip: Think of this as your “glowing letter of recommendation” for buying a home. It moves you to the top of the offer pile when competing with other buyers.

Here's what it looks like in a California Purchase Agreement. You'll see all 3 levels boxed on the right.

Here's what it looks like in a California Purchase Agreement. You'll see all 3 levels boxed on the right.

So... Which One Should You Choose?

Here’s a quick cheat sheet:

| You Are... | Best Option |

|---|---|

| Just exploring | Pre-Qualification |

| Buying in 3–6 months | Pre-Approval |

| In a hot market / Complex income | Fully Underwritten Pre-Approval |

Still unsure where to start? Use my free Home Affordability Calculator or check out my 12 Month Homebuying Playbook. Or if you're looking sooner, here's Buying a home in 90 Days (Full Gameplan).

Main Takeaway

Whether you’re just browsing Zillow on your lunch break or gearing up to make an offer next month, the type of approval you choose matters.

Do the prep now, win big later. You don’t need all the answers today just the right guide.

Keep stacking the wins,

Nathan